Giving and Receiving: Understanding the Financial Flows Between Young People and Their Parents

Scale2Save Campaign

Micro savings, maximum impact.

Editor’s note: This article is part of NextBillion’s series “Enterprise in the Time of Coronavirus,” which explores how the business and development sectors are responding to the pandemic. For news updates and analysis, virtual events, and links to useful resources related to the COVID-19 crisis, check out our coronavirus resource page.Last year I was part of a team that conducted a Financial Diaries study of young people in Morocco, Nigeria and Senegal as part of a comprehensive research project on “Young People in Africa” that was conducted on behalf of the Scale2Save Programme — a partnership between the World Savings and Retail Banking Institute and the Mastercard Foundation. The team has produced a comprehensive report on our findings, but we also wanted to share some of what we learned in a more accessible format, and to explore the implications in light of COVID-19. This is the first of three NextBillion articles coming out of that study – you can read the second article here, and the third one here.

Young people in Morocco, Nigeria and Senegal tend to live in their parents’ homes until around 25 years of age. They maintain a strong connection to their parents when living at home, and that bond remains when they move away. In this context, parents often provide financial and other support to their children. But is this always the case? And if not, what are the implications for financial service providers and financial inclusion promoters?

In this study we asked young people to tell us about any support they had given or received from various members of their family, as well as friends and neighbors. The answers suggest a complex, dynamic interplay between parents and their children that extends beyond a one-way dependency of young people on their parents – especially among the Morocco sample of young people.

In the face of the COVID-19 pandemic and the lockdowns it entails, opportunities for young people to earn money have been hit hard – and their parents are facing similar challenges. We do not know the ultimate impact of the pandemic on families, but the financial diaries data we’ve gathered suggest that it will affect both the economic activities of individual family members and the economic relationships among family members.

CONTEXT MATTERS

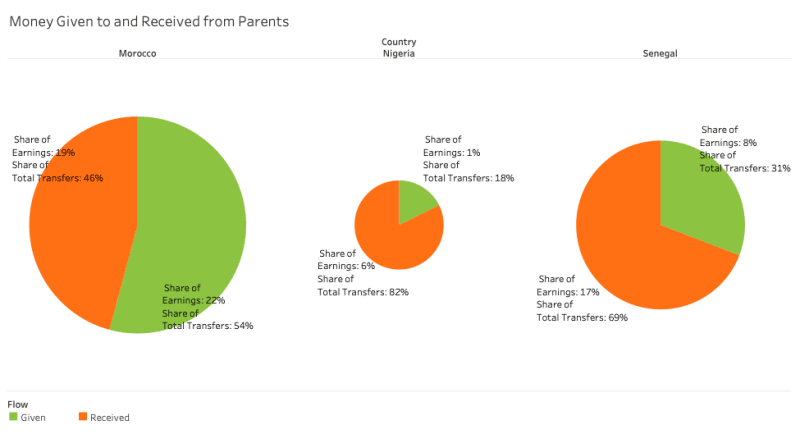

There was considerable variation in the amount of money young people gave to or received from their parents during the study. This variation may not be generalizable to the young people in the country as a whole because of the small sample size, but it is indicative of how different parent-child financial relationships can be. For instance in Morocco, young people gave more to their parents than they received, while in Senegal young people gave less than half what they received from their parents. In Nigeria, it was less than a quarter. Furthermore, in Morocco transfers of money were far greater as a share of the total earnings of participants in the diaries studies: Transfers there amounted to 41% of the participants’ earnings, while in Senegal they were 25%, and in Nigeria only 7% (Figure 1).

In Figure 1 the size of each pie shows the total amount of transfers as a share of earnings—the bigger the pie, the bigger the amount of transfers relative to the respondents’ earnings – while the slices of the pie show the share of transfers received by the diaries participants and the share of transfers they gave.

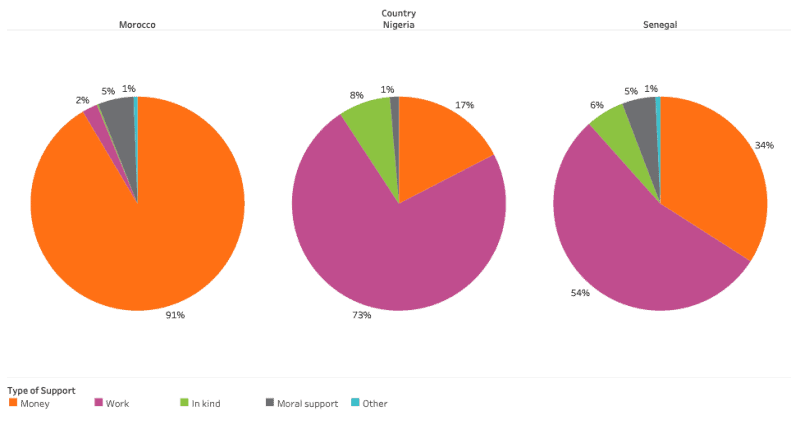

These financial support patterns should be seen in light of the overall support that young people receive and give. For example, the Moroccan young people overwhelmingly reported giving their parents financial support as opposed to in-kind or work support. In contrast, in Nigeria, young people only gave financial support in less than 20% of all instances when they gave their parents support. In most instances, they supported their parents with work. In Senegal, 34% of instances were in the form of money and 54% in the form of work (Figure 2).

Figure 2: Type of Support Given by Young People to their Parents

MOTHERS MATTER

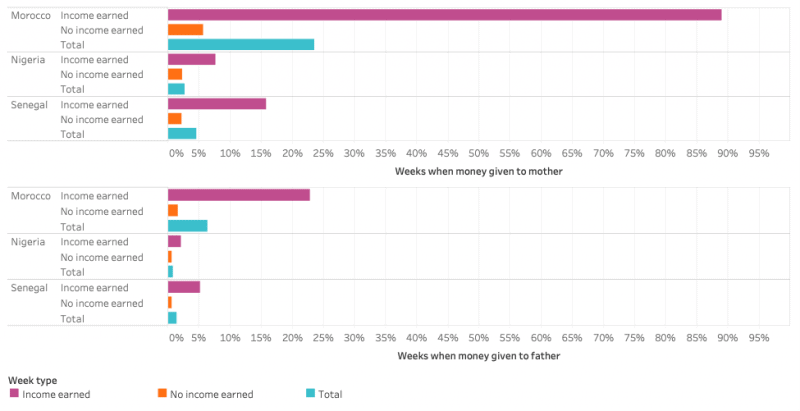

Generally, young people in each country worked or participated in a business activity about half the time or less: 46% of the time in Morocco, 52% of the time in Nigeria, and 34% of the time in Senegal. But when they did work, they gave money to their parents, especially their mothers and especially in Morocco — in almost every week that they worked, young Moroccans gave money to their mothers. In contrast, they only gave money to their fathers in less than a quarter of the weeks when they worked. Young Senegalese and Nigerians were generally less likely than young Moroccans to give money to their parents in weeks when they earned, but, as in Morocco, mothers were still their priority (Figure 3) when they did give money to their parents.

Figure 3: Share of Weeks when Money Given to Parents, by Week Type

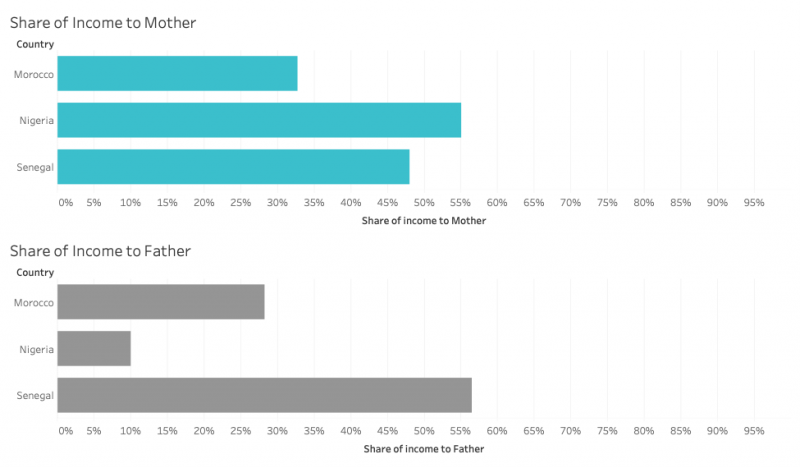

Finally, we are able to use the diaries data to see how much of their income young people gave to their parents in weeks when they did give them money. We calculated the amount they gave as a share of their reported earnings during the week when they gave money. As shown in Figure 4, the data suggest that in Morocco, when young people gave money to their mothers, it constituted about one-third of their income for that week. The same was true when they gave money to their fathers — but note that they gave to their fathers far less often, hence the total they gave to them was less. In Senegal, when young people gave money to either their mother or father, they gave around half of their earnings. In Nigeria, they gave about half of their earnings to their mothers, when they did give money, but little of their weekly earnings to their fathers. But, again, it is important to remember that these calculations are just for weeks when a young person gave money.

Figure 4: Share of Weekly Income Given to Parents During Weeks when Young People were Working

GIVING: A TWO-WAY STREET BETWEEN PARENT AND CHILD

The data on the behaviors of the groups of young people in the countries covered by the financial diaries study suggest a wide variety of relationships between young people and their parents. This may have something to do with the differences in the cultures of the three countries, but it may also have something to do with differences in sampling—i.e.: who we were able to talk to and the type of communities they lived in—across the countries.

In a nutshell, the data show how young people support their parents, both financially and through work and in-kind gifts, as well as how they receive support from their parents. In the case of young people in Morocco, the amount given exceeded the amount received, and their giving was common and frequent and constituted a third of their earnings (when they did earn). In Nigeria and Senegal, young people were more likely to support their parents by working for them. In the time of COVID-19, economic resilience is more important than ever. Depending on which generation in a family is most adversely affected by the pandemic, we would expect the other generation to increase their support. In many families we’d expect young people to play a critical role in strengthening family resilience through the support they give to their parents. On the other hand, in cases where young people have been disproportionately hit, we’d expect parents to step up their support for their children, whether they’re still living at home or not.

What does this suggest for financial service providers and others interested in promoting financial inclusion? One key takeaway is that taking a close look at the relationship between young people and their parents – and especially their relationship with their mother – can help providers work out the best ways to connect young people to financial institutions. This raises the question: Could mothers become allies in promoting the accumulation of savings in a young person’s bank account, in the purchase of health insurance, or in the use of other types of financial services? In the next two articles in this series, we’ll discuss these questions – and explore ways that providers can strengthen the resilience of families in the context of COVID-19 by making it easier for money to flow among family members in mutual support of each other.

Scale2Save

Young people matter: A case study from FCMB in Nigeria

Scale2Save Campaign

Micro savings, maximum impact.

Nigeria can best be described demographically as a youth country, with a rich culture of young people who are agile and highly ambitious, however, that youthful population faces a lot of financial insecurity, expensive educational degrees, and unemployment. Given this, FCMB saw vast opportunities with this population and, developed in 2016 the “Flexx” programme. The goal was to make financial matters – and understanding concepts around them – as interesting as possible, addressing the uncertainties of the future with a sound financial and investment knowledge that will impact people’s futures.

Scale2Save partner empowers youth through financial education programme.

>> The incredible journey of #FCMBFlexxterns

>> Sights and sounds from the #FCMBFlexxtern ‘Meet and Greet’

>> Dare2Dream Kinabuti Talenthunt, Benin

BRUSSELS, 12 August 2020 — Nigeria can best be described demographically as a youth country, with a rich culture of young people who are agile and highly ambitious, however, that youthful population faces a lot of financial insecurity, expensive educational degrees, and unemployment. Given this, FCMB saw vast opportunities with this population and, developed in 2016 the “Flexx” programme. The goal was to make financial matters – and understanding concepts around them – as interesting as possible, addressing the uncertainties of the future with a sound financial and investment knowledge that will impact people’s futures.

Younger market grows in importance:

A report published in 2018 by EFINA, a financial sector development organisation, shows that the youth segment defined by them – between the age of 18-35 – numbered 56.7 million, with only 21.5 million having a bank account. That means 62% had no bank account and 38.7% were financially excluded. FCMB knows this youth segment cannot be ignored, and aim to attract young people to FCMB.

FCMB’s Executive Director, Retail Banking, Mr Olu Akanmu said: “It’s always best to keep up with the times by targeting a younger, more technologically savvy demographic that can bring many benefits to FCMB. Those benefits include an active drive for innovation, the “humanisation” of banking procedures and operations and the goodwill of a growing market.”

FCMB’s Executive Director, Retail Banking, Mr Olu Akanmu said: “It’s always best to keep up with the times by targeting a younger, more technologically savvy demographic that can bring many benefits to FCMB. Those benefits include an active drive for innovation, the “humanisation” of banking procedures and operations and the goodwill of a growing market.”

Image: Dare2Dream Kinabuti Talenthun event in Benin City

Teenagers and young adults: The “future” looking someday for a place to bank their money

Teenagers and youth adults today, but eventually, they become valuable and active members of the economy and digital world. To be able to attract them to FCMB, the microfinance bank had to come up with the “Flexx” programme that presents the bank in the right way, with a youthful brand identity and by taking part in driving financial Inclusion by becoming a more friendly and accessible bank.

To succeed in a market that will be dominated by Millennials and Gen Z-ers, FCMB had to be more “sociable” and seen as approachable. Knowing this group of people were digital natives, FCMB had to go in deep and meet them on their turf – in cyberspace.

Youth understand the value of money, will try to save it

Gaining consciousness just at the time when the financial crisis struck, and seeing the effects of the economic downturn everywhere – loss of jobs and university degrees hanging in the balance – money became a prime concern for this generation of FCMB customers. We have the unique opportunity to help reach out and be seen as a “partner” to help them navigate through the financial woes.

Image: FCMB Flexxtern Meet and Greet.

First in addressing the needs of financial inclusion we had to remove the barriers to entry and opening a bank account, this we developed the Easy Account which enables the youth to have a basic entry bank account with just their mobile phone number (>>See related video), then we had to ensure the youths understand simple money matters by creating a digital savings platform that enables them to save towards a goal and plan on a daily, weekly or monthly basis. The aim is to let them inculcate a healthy savings and investment habit. And lastly, a digital zone was created to constantly keep them engage with contents that are germane to them.

Youths have pushed FCMB to innovate ahead of competitors

FCMB have been catering to the youths who are more technology-proficient than their predecessors, through various digital engagement which include the following:

- Flexx zone with over 130,000 visits and Flexx Mobile App with 17,329 users.

- Dare to Dream talent hunt in 10 campuses and over 15,000 participants in the three-year span.

- Flexx your creativity that had close to 20,000 digital reaches; this was a digital showcasing of their creative art.

- Flexxtern in partnership with Lagos State Government, corporate and SMEs, providing internship opportunities to youth in structured organisations.

- YEEP- Youth Entrepreneurship Programme for National Youth Service Corps (NYSC), with the participation of over 20,000 corps members in the last two years.

- Youth Entrepreneurship Masterclass which has provided the opportunity for young entrepreneurship to acquire more knowledge and mentorship in various field.

- National Youth Service Corps (NYSC) camp engagement in at least 20 states for the last four years reaching more than 300,0000 corps members in orientation camps.

- Weekly campus activation to engage young people in different institution of learning on the need to save during and after school. This provides an opportunity for financial inclusion and enlightenment.

Image: FCMB meet with young people who are contestants in a youth competition

Scale2Save, partners celebrate International Youth Day International Youth Day on 12 August presents an opportunity for Scale2Save partners like FCMB in Nigeria to showcase their stories. That includes how partners serve and empower youth and young people through their projects. Project partner share stories from real people who benefit from their efforts to raise awareness around the need to mobilise savings among – and strengthen the resilience of – low-income populations, which includes financially excluded youth and young people.

International Youth Day on 12 August presents an opportunity for Scale2Save partners like FCMB in Nigeria to showcase their stories. That includes how partners serve and empower youth and young people through their projects. Project partner share stories from real people who benefit from their efforts to raise awareness around the need to mobilise savings among – and strengthen the resilience of – low-income populations, which includes financially excluded youth and young people.

The campaign matters because interest exists within governments, NGOs and international bodies to learn more about how financial institutions address the needs of youth, young people and young adults. For example, financial inclusion features in eight of the 17 UN Sustainable Development Goals. This year’s International Youth Day theme, “Youth Engagement for Global Action”, seeks to highlight ways in which engagement of young people at local, national and global levels enriches national and multilateral institutions and processes, the UN says. It also draws lessons on how their representation and engagement in formal institutional politics can be boosted.

WSBI, Scale2Save and youth research

WSBI’s Scale2Save programme conducts research on youth and young people in Africa. To learn more visit the Scale2Save website.

Scale2Save

Resilience, sustainable banking models through savings

Scale2Save Campaign

Micro savings, maximum impact.

WSBI will lead on 11 August a SEEP Network webinar session on the needs of bank customers, which remains a challenge in Africa.

>> Learn more about Scale2Save

>> See Scale2Save research paper (.pdf)

>> Register now for SEEP-hosted webinar

BRUSSELS, 4 August 2020 – WSBI will lead on 11 August a SEEP Network webinar session on the needs of bank customers, which remains a challenge in Africa.

Based on findings of a recent Savings and Retail Banking in Africa report published in February by Scale2Save, the session will present key insights from it and discuss major challenges to encourage savings for low-income customers. Structured on four pillars of financial inclusion – usability, affordability accessibility and sustainability – different perspectives from both the demand and supply side will be discussed. In addition, presenters will share early findings from the 2020 research assessing the impact of the COVID-19 pandemic on banks in Africa.

SEEP is a collaborative learning network whose members for more than 30 years have served as a testing ground for innovative strategies that promote inclusion, develop resilient markets, and enhance the livelihood potential of the worlds’ poor. The webinar is hosted by the SEEP Network in partnership the Mastercard Foundation Savings Learning Lab, a six-year initiative implemented by Itad, in partnership with the SEEP Network, that supports learning among the Foundation’s current savings sector portfolio programmes: WSBI’s Scale2Save and Savings at the Frontier.